Did you know that 87% of U.S. companies making over $100 million a year are still privately owned?

Source 1

Crazy, right?

But here’s the thing — almost all the attention (and headlines) go to the other 13%: the ones on the stock market.

Meanwhile, the private market has been quietly outperforming with higher returns, lower volatility, and stronger diversification — especially when the public markets get rocky.

Source 2,3,4

Why don’t more people know about this?

Because for a long time, regular investors weren’t allowed in. Private investments were mostly off-limits — reserved for big institutions and the ultra-wealthy.

But that’s starting to change.

Right now, there might be a rare window of opportunity to get in before the rest of the crowd catches on.

In this post, I’ll walk you through 5 key reasons why private market investing is such a hidden gem.

Especially if you’re a high-net-worth engineer thinking about retirement — and why 2025 could be the perfect time to explore it.

So… what is private market investing, exactly?

In simple terms, it means putting your money into companies or projects that aren’t traded on the stock exchange.

Instead of buying shares in Apple or Amazon, you’d be looking at things like:

Private equity – owning part of a private company

Private credit – lending money directly to businesses

Private infrastructure or real estate – investing in things like roads, data centers, or apartment buildings

Until recently, these kinds of opportunities were out of reach unless you had millions to invest.

But not anymore.

Here are 5 reasons why now might be the smartest time to take a serious look.

1. The Traditional Portfolio Might Not Cut It Anymore

For decades, the classic 60/40 portfolio (60% stocks, 40% bonds) has been the go-to retirement strategy.

And for good reason:

Stocks grow your money for the long term

Bonds give you steady short-term income

When one goes down, the other (usually) goes up

But we’re not living in the same economy anymore.

These days, bond yields are often stuck around 2–4%.

Which barely keeps up with inflation, let alone builds real wealth.

Source 5

Worse, stocks and bonds aren’t always balancing each other out like they used to (just think back to 2022 — both took a hit ).

Source 6

And with people living longer — some well past 100 — retirement money needs to stretch further and last longer than ever before.

This is where private markets can step in.

2. Most Growth Happens Before Companies Go Public

Ever hear someone say, “I wish I’d invested in Uber or Airbnb early on…”?

Hate to break it to you, but by the time those companies went public… it was already too late.

Most of the real growth happened while they were still private. And that’s actually by design.

Source 7

A lot of startups stay private as long as they can so they can grow quietly, without the pressure of public shareholders or all the red tape that comes with being a public company.

Staying private gives them more control, fewer rules, and the space to scale on their terms.

Then, when they finally do hit the public market, the company is already worth a fortune — and the early investors have already made their money.

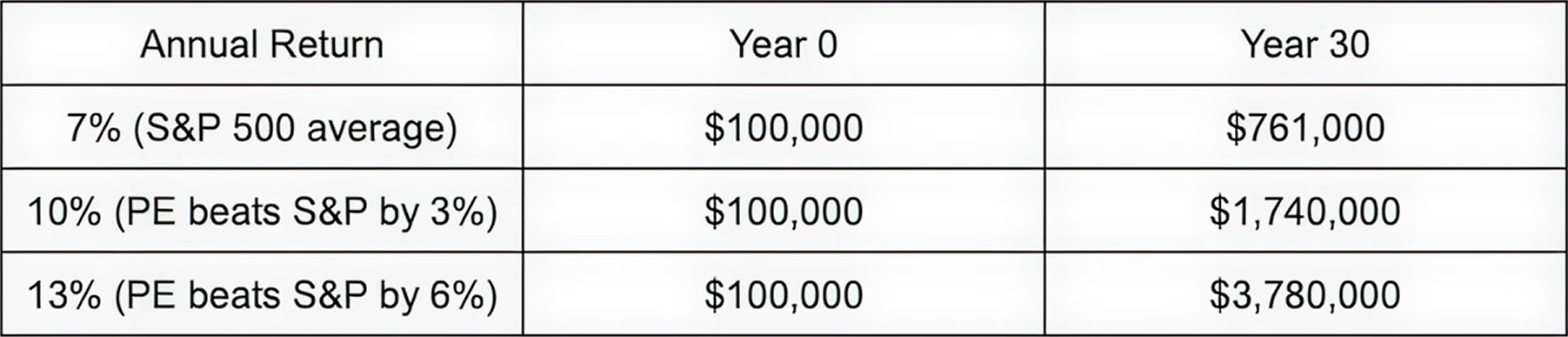

That’s why a recent study from 2024 by the CAIA Association found that, over the long haul, private equity has generally outpaced the S&P 500 by about 3% to 6% per year.

Source 8

3% to 6% might not sound like much—until you look at what it does over time:

That’s the power of compounding.

Just 3% more can more than double your return.

6%? You’re looking at almost 5X.

3. Not All Diversification Is Real Diversification

Many portfolios look diversified on paper—some stocks, a few bonds, maybe even a bit of real estate.

But here’s the thing: if everything drops when the stock market drops… is it really diversified?

That’s where private assets come in.

They often zig when public markets zag—especially during recessions or times of volatility.

Take private credit, for example.

It’s basically lending money to businesses outside the traditional banking system.

And it’s been quietly delivering steady, sometimes even double-digit returns, even when the stock market is flat or falling.

Source 9

That’s because:

It isn’t priced daily by panicked markets

Its value is based on cash flow and fundamentals—not headlines

It can keep generating income even when public markets are down

Many portfolios look diversified on paper—some stocks, a few bonds, maybe even a bit of real estate.

But here’s the thing: if everything drops when the stock market drops… is it really diversified?

That’s where private assets come in.

They often zig when public markets zag—especially during recessions or times of volatility.

Take private credit, for example.

It’s basically lending money to businesses outside the traditional banking system.

And it’s been quietly delivering steady, sometimes even double-digit returns, even when the stock market is flat or falling.

That’s because:

4. Lower Volatility, Less Stress

The public market is volatile, emotional, and increasingly manipulated by algorithms, politics, and media hype.

Just look at Tesla over the last 6 months — it’s been all over the place.

And what happens?

Most investors get caught up in the noise.

They buy high, panic when things dip, and sell low. That’s why, even though the market averages around 10% a year, the average investor ends up making just 4.25%.

Source 10,11

Private investments work a little differently.

They’re not priced every second.

You can’t just sell them at the click of a button.

And honestly? That’s a good thing.

It helps take the emotion out of investing — which most people don’t realize is half the battle.

The result? Private market investors often completely avoid these costly market timing mistakes, potentially saving them hundreds of thousands of dollars in the process.

All that without having to check the news every morning.

5. Perfect Timing

Private investing used to be this exclusive club — reserved for institutions, billionaires, and people with insider connections.

To even get in the door, you often needed $250,000 or more — sometimes even millions.

And even then, the best deals were quietly passed around in exclusive circles. If you weren’t “in the room,” you didn’t even know these opportunities existed.

Why so secretive? Mainly because the returns were so lucrative that the people at the top wanted to keep the pie to themselves.

But that’s changing. And it’s changing fast.

Through some of the connections I’ve built over the years, I’ve been lucky to get access to some really interesting private market deals.

And I’m not the only one. More financial advisors and individual investors are starting to explore this space too.

The good news? It’s still relatively early.

These opportunities aren’t overcrowded yet, so there might be a real chance to find great deals, better entry points, and invest in things that usually stay behind closed doors.

Now, we’re at a real turning point.

And luckily, 2025 is shaping up to be a sweet spot to get in:

Private equity is picking up momentum

Real estate is stabilizing after recent corrections

Private credit and infrastructure are booming, especially in areas like AI and clean energy

Source 12,13,14

Put simply, 2025 could potentially be a smart time to enter—before the next wave of growth begins and the regular investors flood the market.

What to Watch Out For?

Private market investing can be really exciting and rewarding, but it’s not without its challenges.

For one, your money usually isn’t easy to get out quickly. These investments tend to be “locked up” for several years, so it’s important to plan ahead.

They can also come with higher fees than regular stocks or bonds on the public market.

Returns can be great, but they’re never guaranteed — there’s always a chance you could lose money.

Because private deals aren’t as tightly regulated or transparent, it’s important to really understand what you’re getting into.

So before diving in, think about your goals, how much risk you’re comfortable with, and have a good chat with a financial pro who knows the space well.

Curious about how private market investing could fit into your retirement plan?

I’m offering a free, no-pressure strategy call where we can walk through your goals and see if this kind of investing makes sense for you.

Especially with the unique opportunities emerging in 2025.

There’s zero obligation, no sales pitch, and definitely no strings attached.

Just a relaxed, educational conversation with me to help you get clarity — and maybe even uncover options you didn’t know existed.

Book your free call here.

You’ve engineered everything else with precision. Why not your wealth?

Sources:

Sløk, Torsten. Many More Private Firms in the US [online]. New York: Apollo Academy, 2024 [accessed 2025-06-13]. Available at: https://www.apolloacademy.com/many-more-private-firms-in-the-us/?utm_source=chatgpt.com

Cheng, Joseph & Farook, Yaser. Re‑thinking Private Equity Risk and Reward for LP Allocations [online]. Fontainebleau: INSEAD Global Private Equity Initiative, 2020 [accessed 2025‑06‑13]. Available at: https://www.insead.edu/sites/default/files/assets/dept/centres/gpei/docs/re-thinking-pe-risk-and-reward.pdf?utm_source=chatgpt.com

Financial Times. Private market funds lag US stocks over short and long term [online]. 2025. Available at: https://www.ft.com/content/c21a5ca9-6175-498a-bf32-9c91e4366085 [Accessed 13 Jun. 2025].

Blue Owl. Diversification Benefits of Private Markets [online]. 2024. Available at: https://wealth.blueowl.com/learnengage/bo-diversification-benefits-private-markets [Accessed 13 Jun. 2025].

MarketWatch. You Want Income in Retirement, But Soaring Bond Yields Can Be Risky — What Should You Do? [online]. 2024. Available at: https://www.marketwatch.com/story/you-want-income-in-retirement-but-soaring-bond-yields-can-be-risky-what-should-you-do-b222661d [Accessed 13 Jun. 2025].

Morningstar. Why the Bond Market Looks Brighter Than It Did in 2022 [online]. 2025. Available at: https://www.morningstar.com/bonds/why-bond-market-looks-brighter-than-it-did-2022 [Accessed 13 Jun. 2025].

Hamilton Lane. Private Market Investing: Staying Private Longer [online]. 2022. Available at: https://www.hamiltonlane.com/en-us/insight/staying-private-longer [Accessed 13 Jun. 2025].

CAIA Association. Long-Term Private Equity Performance: 2000 to 2023 [online]. 2024. Available at: https://caia.org/blog/2024/04/23/long-term-private-equity-performance-2000-2023 [Accessed 13 Jun. 2025].

Deutsche Bank. Private Credit – A Rising Asset Class Explained [online]. 2024. Available at: https://flow.db.com/trust-and-agency-services/private-credit-a-rising-asset-class-explained [Accessed 13 Jun. 2025].

Virtus Investment Partners. Minds Over Markets: A Behavioral Guide to Investing [PDF]. 2024. Available at: https://www.virtus.com/assets/files/35y/minds-over-markets_5500.pdf [Accessed 13 Jun. 2025].

Boomer & Echo. How The Behavior Gap Affects Investor Returns [online]. 2014. Available at: https://boomerandecho.com/behavior-gap-affects-investor-returns/ [Accessed 13 Jun. 2025].

EY. Private Equity Pulse: Key Takeaways from Q1 2025 [online]. 2025. Available at: https://www.ey.com/en_us/insights/private-equity/pulse?utm_source=chatgpt.com [Accessed 13 Jun. 2025].

MSCI Inc. Real Estate in Focus: 2025 Trends to Watch [online]. 2025. Available at: https://www.msci.com/research-and-insights/blog-post/real-estate-in-focus-2025-trends-to-watch?utm_source=chatgpt.com [Accessed 13 Jun. 2025].

Paul, Weiss, Rifkind, Wharton & Garrison LLP. Private Credit: Spotlight on M&A and Infrastructure [PDF]. 2025. Available at: https://www.paulweiss.com/media/rjflsnxx/part_ii_private_credit_spotlight_on_ma_and_infrastructure.pdf [Accessed 13 Jun. 2025].

Disclosures & Disclaimers: This content is for informational and educational purposes only and does not constitute financial, investment, or legal advice. It does not represent an offer to buy or sell any securities. Private market investments are speculative, typically illiquid, and involve a high degree of risk, including the potential loss of principal. They are generally suitable only for accredited investors and may require long holding periods and limited liquidity. Any historical performance figures mentioned are illustrative, not guaranteed, and may not reflect actual results. All investing involves risk. Before making any investment decisions, consult with a qualified financial advisor who understands your specific situation, goals, and risk tolerance.